New CFPB Integrated Disclosures

ATG Will Help You Prepare for August Implementation

As the holiday season approaches, the August 1, 2015, implementation date of the Consumer Financial Protection Bureau (CFPB) rule integrating the TILA-RESPA disclosures is only nine (9) months away.

The rule consolidates four existing disclosures into two forms: the Loan Estimate and the Closing Disclosure.

The rule applies to most closed-end consumer credit transactions secured by real property. Transactions exempted include:

- Home equity lines of credit;

- Reverse mortgages;

- Mortgages secured by a mobile home or dwelling not attached to land; and

- Loans made by a creditor who makes five or fewer mortgages per year.

Significant Changes

Zero Tolerance – The fees paid to the lender, mortgage broker, or an affiliate of either may not increase from what is disclosed on the Loan Estimate. The fees paid to an unaffiliated third party may not increase if the lender does not permit the consumer to shop for that service. Transfer taxes are also subject to a zero tolerance.

10% Cumulative Tolerance – Recording fees and fees paid to third-party service providers, when the lender allows the consumer to shop and the consumer selects a provider on the creditor’s written list, are subject to a 10% cumulative tolerance.

Charges Not Subject to a Tolerance – Prepaid interest, property insurance premiums, escrows, and services required by the lender when the consumer is allowed to shop. When the consumer selects a third-party provider not on the creditor’s written list of service providers, the fee for that service is not subject to a tolerance.

Closing Disclosure - What’s New?

- Itemization is back and roll-up lines are gone.

- Agent/underwriter split for title premiums is no longer required.

- Seller’s title charges assessed to the buyer are gone.

- Line numbers are gone, fees will be alphabetized.

- Owner’s Title Insurance is listed as “Optional.”

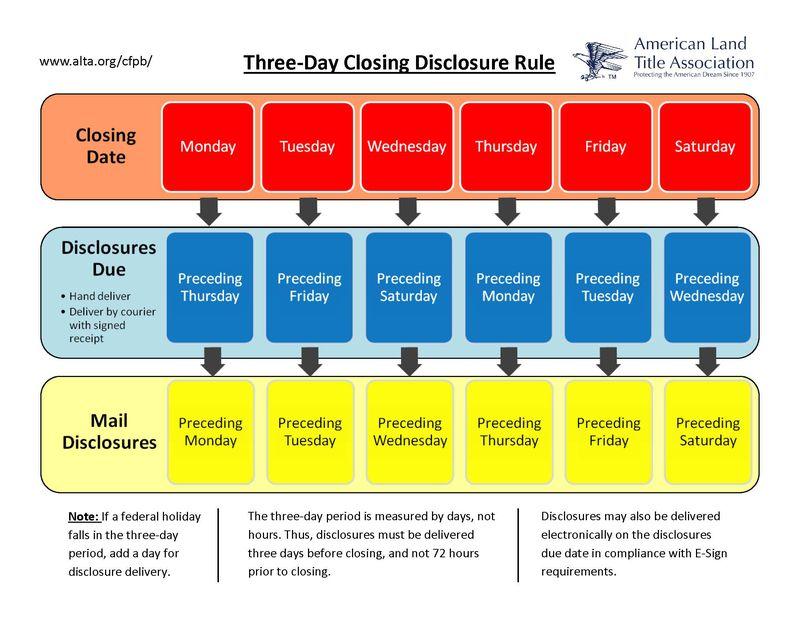

The Closing Disclosure replaces the HUD-1 and the final TIL disclosure. The rule requires the creditor to provide the Closing Disclosure to the consumer (borrower) three business days before consummation. Consummation occurs when the consumer becomes contractually obligated to the creditor on the loan – basically, the closing when the consumer executes the note and mortgage.

The creditor is responsible for the completion and timely delivery of the Closing Disclosure, however, the CFPB has acknowledged the significant role of settlement agents in the closing process and allows creditors to contract with settlement agents regarding completion and delivery of the disclosure.

Delivery Three Business Days Prior to Consummation

The consumer must receive the Closing Disclosure three business days before the closing. The Closing Disclosure may be delivered in person, by mail, or by other delivery methods including email. Electronic delivery methods are subject to compliance with consumer consent and the Electronic Signatures in Global and National Commerce Act. Wells Fargo has announced that they will complete and deliver the Closing Disclosure. They’ve also indicated that they intend to utilize US mail to deliver the disclosure. Delivery by mail under the rule is presumed to occur three business days after posting. This means the completed disclosure, containing figures from all parties, must be placed in the mail preferably 10 days prior to the closing date to meet the three-day rule and allow for non-business days, such as Sundays. Lenders utilizing this method of delivery will obviously need to schedule their closings far in advance and they’ll need figures from all parties to the transaction in order to complete and deliver the Closing Disclosure.

The rule defines a business day as all calendar days except Sundays and the legal public holidays specified in 5 U.S.C. 6103(a).

| 2015 Federal Holiday Schedule | |

|---|---|

| Date | Holiday |

| Thursday, January 1 | New Year’s Day |

| Monday, January 19 | Martin Luther King, Jr.'s Birthday |

| Monday, February 16 | Washington’s Birthday |

| Monday, May 25 | Memorial Day |

| Friday, July 3* | Independence Day |

| Monday, September 7 | Labor Day |

| Monday, October 12 | Columbus Day |

| Wednesday, November 11 | Veterans Day |

| Thursday, November 26 | Thanksgiving Day |

| Friday, December 25 | Christmas Day |

| *July 4, 2015 falls on a Saturday. For most Federal employees, Friday, July 3, will be treated as a holiday. | |

Changes that require a new disclosure and an additional three-business-day waiting period after receipt have been limited to the following:

- changes to the APR above 1/8 of a percent for most loans and 1/4 of a percent for loans with irregular payments or periods;

- changes to the loan product; and

- the addition of a prepayment penalty to the loan.

Waiving the Three Business Day Waiting Period

Consumers may waive or modify the waiting period when:

- the extension of credit is needed to meet a bona fide personal financial emergency;

- the consumer has received the Closing Disclosure; and

- the consumer gives the creditor a dated written statement that describes the emergency, specifically modifies or waives the waiting period, and bears the signature of all consumers who are primarily liable on the legal obligation.

Seller’s Closing Disclosure

The settlement agent is required to provide the seller with the Closing Disclosure no later than the day of consummation. If the Closing Disclosure provided to the consumer also contains the seller’s information a copy may be provided to the seller. If the settlement agent provides the seller with a separate disclosure a copy of the seller’s disclosure must be provided to the creditor.

Title Insurance Charges on the Loan Estimate and Closing Disclosure

The rule requires that when owner’s and lender’s policies are simultaneously issued, the full, undiscounted rate should be disclosed to the consumer on the Loan Estimate and the Closing Disclosure. The Owner’s Title Insurance is to be disclosed in the “Other” category and is to be calculated by adding the simultaneous issuance premium to the full owner’s policy premium, and then deducting the full premium for the lender’s coverage. In the majority of states this results in overstated title charges to the buyer and an inflated cash to close figure. Consequently, the seller’s title charges and proceeds will be understated. The American Land Title Association and The Mortgage Bankers’ Association have both written to the CFPB to comment on this issue in hopes of having the rule amended.

Uniform Closing Dataset (UCD)

The Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac) have created a Uniform Closing Dataset (UCD) to standardize the naming of fees used for loans they purchase. Since the Closing Disclosure requires fees to be listed alphabetically, the UCD will greatly simplify the data entry process by requiring uniform use of such terms as Realtor commission, recording fees, etc. Fannie and Freddie expect to begin requiring use of the UCD in 2016.

Software and Training for ATG Staff and ATG Agents

To stay informed on this important topic, ATG mangers and staff have attended CFPB webinars, ALTA webinars, and webinars on the CFPB rule offered by RamQuest®. We will offer training opportunities for ATG agents in 2015, but until then we strongly recommend ATG agents and their employees view our 2014 OnDemand program, The New Real Estate Closing Process: CFPB Rule Explained. We will announce our plans for additional, specific training for ATG agents, closers, and staff in the spring of 2015, after the new software is released (expected in the first quarter of 2015). Watch your email and our website for details.

Conclusions

It is evident from the content of this rule that the CFPB is primarily focused on borrowers and lenders. The CFPB wants to ensure that consumers can obtain a mortgage through a process that is without surprises. However, this rule is only one of many new regulations impacting lenders and the processes they use to originate and service mortgages. Lenders have the liability and will determine the settlement agent’s role in the preparation of the Closing Disclosure. This presents a unique opportunity for all of us to reach out to the lenders and Realtors in our areas to become their trusted advisers and partners on the implementation of the Integrated Disclosures.

As always, our goal is to ensure that attorney agents remain part of the title insurance landscape by offering support and tools to help you comply with the CFPB rule and ALTA Best Practices. We appreciate that certain components will be a challenge. Take advantage of the tools and information on our website and upcoming training programs to ease the transition. Contact us with questions or concerns. We look forward to hearing from you.

David S. Huffman

ATG Senior Vice President - Title Operations

[Last update: 12-8-14]

Print this page

Contact Us

Contact Us HelpDesk

HelpDesk Email Us

Email Us